PPO Strategies to Get the Best Dentistry for Patients.

It is no secret that dentists are feeling the financial pain of preferred provider organization (PPO) participation. In some states, dentists must agree to discount their fees up to 80 percent in exchange for being listed as a “Preferred Provider” (in-network).

I recently referred my brother to a local dentist. After having a crown seated on tooth number 30, my brother complained about the lack of quality in the dentist’s work. Surprised, I investigated the issue to understand what had happened.

I discovered that the dentist I recommended had an internal policy to only use certain dental laboratories, depending on the reimbursement structure that the patient’s PPO offered. As a result, my brother’s low-reimbursing PPO led to a low-cost crown that fractured just 10 days after it was seated.

While some people might claim that the dentist was committing fraud by not using the best quality dental lab (and was therefore providing suboptimal care for the patient), the dentist had valid financial reasons for using a discount dental lab.

I learned that this dentist actually lost money with some PPO reimbursements. Using lower-cost labs for the PPOs that required steeper discounts was strictly a business decision, and not a sneaky strategy to provide low-quality care in hopes that the patient wouldn’t notice the difference.

Having known this dentist for several years, I understood his dilemma. He is an honest and trustworthy person who was merely trying to make the numbers work at the end of the day. I believe he was innocently misguided by the perceived rules and regulations of PPO participation.

I place the blame entirely on the insurance industry for driving a so-called “insurance mentality” that causes many dentists to forego quality or conservative dentistry in an effort to sustain a viable dental business.

INSURANCE MANDATES

Even though some insurance plans allow dentists to charge a lab fee to the patient directly, the allowed charges are often at levels that only cover very basic lab work or other materials. A huge disconnect between dental insurance companies and dentists is that insurance companies usually have no idea what it costs to deliver high-quality dentistry. I once attended a dinner with two executives from a large insurance company who openly confessed that they had no idea how much it costs for a doctor to perform clinical procedures. They said, “Our company simply doesn’t care.”

During this meeting, the executives talked about the rights and options of doctors and patients when it comes to denied claims, and even suggested strategies for patients who seek treatment that is above their coverage standards.

According to both executives, dental insurance (PPO, POS, Indemnity, Capitation, HMO, DHMO, or discount) is only designed to cover the basics. Since most employers look at the total cost of a dental plan, many insurance companies opt only to cover the least expensive dental treatments.

They explained that if a patient chooses to receive a service or procedure that is above and beyond the standard care (referred to by the executives as “added-value” procedures), insurance may only cover the basics. However, covering the basics does not free the patient from the financial obligation to pay for a higher level of care.

In order for a material or service to qualify as one that is an “added value,” dentists must justify that the materials or services they are using/performing are above and beyond the standard scope of service as described in the Code on Dental

PROCEDURES AND NOMENCLATURES (CDT)

As an example, D2740 is described as a porcelain all-ceramic crown. A dentist may present an E.max crown to a patient, but the aesthetic components of E.max are not described in the CDT, even though E.max is a porcelain, all-ceramic crown. Therefore, the justifiable added-value components of E.max are the aesthetic/cosmetic properties of this type of crown.

Here’s an example of what an insurance company can do: a dentist billed insurance for a two-surface composite filling. The insurance company downgraded the code to an amalgam two-surface, according to the policy in a standard employer contract. In the contract, the patient is responsible to pay the difference between the cost of the amalgam benefit and the contracted fee for the two-surface composite that was actually placed.

According to the executives, a downgrade—referred to as an alternative benefit on an Explanation of Benefits (EOB)—is not a denial of benefit. It’s simply an election by the patient’s employer regarding what the employer is willing to cover/pay.

LETTING PATIENTS CHOOSE

Another example I discussed with the insurance executives involved a dentist placing several crowns. A patient who fractured several anterior teeth needed crowns on all of them. For this particular patient, D2740 was the standard benefit for anterior teeth. However, the contracted rate between the doctor and the insurance company was 50 percent less than the doctor’s standard fees.

If the patient elected or requested high-quality aesthetics (where material and lab costs equal the contracted fee for D2740 per tooth), would the doctor be obligated to pay out of his or her own pocket for the work? According to the insurance executives, the answer was no.

The doctor was not obligated to take a loss if the patient elected to receive added-value care. Keep in mind that insurance likely only covered the D2740 at the contracted rate, but the higher-end aesthetic materials were fees that the patient was responsible for (according to the contract between employer and insurance).

Here’s where it can become complicated. Often when a dentist calls the insurance company’s provider relations, the person who answers the call does not take the time to research that particular patient’s employer contract. Instead, they give a scripted response that is neither accurate nor truthful and tell the doctor that he or she must stick to the contracted rates only.

Both executives agreed that the problem with provider relations is that they are trained to give the same response for all issues, even though many employers have different contracts and different types of benefit coverage. Provider relations reps steer dental offices in the direction of strictly following the contracted rates for all situations.

The executives explained that their internal systems are designed to benefit the insurance company, not the dentists or the patients. They recommend that, instead of fighting the insurance system, dentists follow any state or federal laws that protect the financial integrity of quality care. They specifically recommended following the federal HITECH Act of 2009 and any state non-covered service laws.

HITECH ACT OF 2009

In 2009, after dental and medical practices began using electronic methods to store patient information, the HITECH Act (a.k.a. the Health Information Technology for Economic and Clinical Health Act) was passed, which mandated that such information be stored securely.

Upon consulting with my attorneys, I learned that HITECH allows patients the right to waive billing insurance for any procedure for any reason. If this right is invoked, the doctor is legally obligated to not bill or disclose the treatment at hand to any party, including insurance.

A doctor can suggest (via a signed consent form) that material fees not be billed to insurance, as they are not covered and may interfere with benefit coverage for any covered services that are a part of the treatment plan. If a patient agrees and signs an insurance waiver for material fees, the insurance company cannot interfere with the patient’s election, and insurance does not need to know about any material charges.

Both insurance executives I spoke with agreed that in an effort to protect the patient’s choice to obtain higher-quality materials and services (which are not covered by the patient’s insurance plan), insurance companies are prohibited from interfering with a patient’s right to pay for them independent of insurance benefits.

STATE NON-COVERED SERVICE LAWS

Nearly 40 states have passed laws that allow doctors to charge their standard office fees for non-covered services. Both insurance executives agreed that while dental lab work is often included in reimbursements for the procedures that require labs, aesthetics and durable materials are not always included.

For example, E.max and most zirconia have aesthetic components to them, and while the American Dental Association (ADA) has advised billing both crown types as D2740, the cost of either crown can vary depending on the level of aesthetic material applied to each.

The insurance executives agreed that if the crown has any added-value work that is above the standard CDT description, the crown may qualify for an additional material fee that the patient can opt to pay for.

In short, aesthetic or durable material fees should be considered added-value treatments in addition to crown treatment, which places the materials in a billable category of their own.

CONSENT FORMS

To comply with legalities, getting written consent from patients should be mandatory. Attorneys and other insurance carriers suggest that doctors always provide written consent when billing material fees or other non-covered services to the patient. One way to be in compliance with laws and avoid the insurance mentality is to ask patients to sign consent forms if they chose to upgrade their dental materials and/or services.

Many insurance waivers include a clause in their contracts stating that patients “acknowledge that procedures or services listed on this consent form are a non-insurance covered service and will not be billed to insurance.” In other words, patients agree (in writing) to pay for non-covered services and procedures on their own.

When a patient signs a release form, it is important for them to understand what it means and that they will not and cannot obtain reimbursement from insurance for those particular procedures or services listed on the form.

It is absolutely possible for dentists to provide high-quality dentistry with high-quality materials independent of PPO provider reimbursement coverage. Dentists can offer higher care for their patients by understanding how non-covered services, material fees, or upgrades can be billed directly to patients.

KNOWLEDGE IS POWER

Each dentist should view this article merely as a suggestion that they consider the strategies I’ve mentioned and do further research on their own. I strongly recommend that dentists first understand their insurance contracts and seek advice from attorneys and other professionals before adding material or upgrade charge policies in their practices.

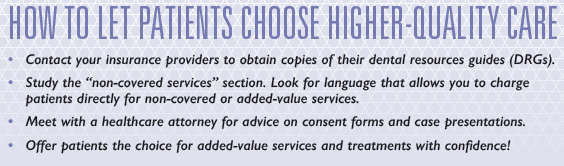

Fortunately, the strategies I’ve outlined are not new. Thousands of dental practices have already implemented similar ones in their own offices. Since following these strategies can entail some liability (depending on the state in which you practice or the PPOs that you participate with), I recommend that you contact each of your contracted insurance providers to obtain copies of their dental resource guides (DRGs).

Study the “non-covered services” section of these DRGs to make sure there is language that allows you to charge patients for non-covered or added-value services.

Next, meet with a healthcare attorney or other professional who can give you advice on areas such as consent forms and case presentations. To avoid losing an insurance audit, it is very important for dentists to understand what needs to be included in a consent form and what not to say to patients when presenting material fees.

Finally, once you are fully prepared to legally and ethically start implementing material fees within your practice, proceed with the utmost confidence. When given a choice, consumers often (and proudly) upgrade to first class airfare, premium fuel for their cars, or even more expensive movie packages that cable/satellite companies offer. Why can’t patients exercise their same rights when it comes to dental upgrades?

It is my hope that dentists will find ways to implement effective strategies to combat the pervasive insurance-driven mentality that is poisoning the dental industry. I sincerely hope each of you will find legal and ethical ways to protect the financial integrity of quality care.