What to Do When Considering Participation with a PPO.

About 15 years ago, our practice, Nankin Dental Associates, in Quincy, MA, participated in a number of PPO programs. As most readers are aware, preferred provider organizations (PPOs) are networks of dentists who participate in the group’s plan at lower-than-customary fees.

At the time, my brother and I were in practice together and we were trying to grow our business. When we signed up for the programs, the reimbursement structure was pretty close to what we were charging, and the fees seemed reasonable.

Over the years, however, many of the fees had become significantly lower than our customary fees, so we stopped participating in several programs. Fortunately, our practice had grown on its own over the years, and ultimately we decided to only participate with the two largest insurance providers in Massachusetts.

A year or so ago, I decided to revisit our PPO participation. At that time, one of the two insurers that we worked with was looking to potentially reduce dental reimbursements by 25 to 30 percent off an already-discounted plan.

The proposed fee decrease was so significant, I knew it would not be worth our time (from a strictly monetary perspective) to continue to treat patients with their insurance at the new rates. I decided to investigate whether options with other providers might be more advantageous.

Our practice was busy, but 35 percent of our patients were covered by this insurer, so we simply could not afford to lose those patients without finding a way to replace them.

I decided to proactively investigate other options because I wanted to remain busy and productive enough to maintain our profitability if the worst scenario happened and we lost 35 percent of our patients.

There’s no shortage of companies that offer these programs—my practice constantly receives solicitations from PPOs. Once or twice a year, they reach out to say that a patient has requested that I participate in their insurance plan. It’s a good way to find insurance companies that are looking to partner with dental practices.

Another company approached a colleague of mine, and he asked if I had ever talked to them. I reached out to the company to see if they were still looking to increase their network, and they were.

After looking at several PPOs, I have learned a few things that dentists can do to ensure that the arrangement is beneficial before entering into an agreement.

1. Look at Productivity

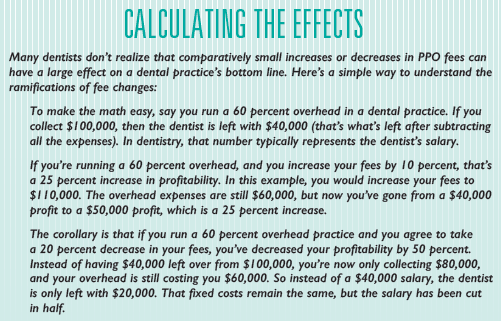

When dentists consider participating in a PPO, they need to know what they’re signing up for, and what the fees will mean to the financial health of the practice. PPO participation can provide great benefits to dentists, such as increased patient and referral flow, but some PPOs may undercut a dentist’s fees, which can cause the practice to flounder and lose money.

Before entering into a PPO agreement, analyze the overall busyness of your dental practice. If the practice is scheduled two to four weeks out with no openings, then it likely doesn’t need to participate in network with an insurance company. A booked schedule means that the practice is able to stay busy while charging full fees, so replacing any of those patients with ones who have discounted PPO fees doesn’t make sense.

However, if a schedule has “holes” in it and a PPO offers fees that allow the dentist to perform dentistry without compromising quality, it might be worth it. It won’t be as profitable as having full-fee patients, but it is better than collecting no money and remaining idle. Dental practice overhead and expenses continue to mount up regardless of the schedule.

Dentists should be aware that filling a schedule completely with PPO patients might limit the time available for scheduling last-minute, full-fee patients. It’s a balancing act that every dentist should consider.

2. Know Your Numbers

Once you have looked at the schedule and determined that the practice could use some new patients, look at your numbers to determine what kind of fees you need. To understand those numbers, you have to know the fixed operational costs for your practice—on an annual, daily, and hourly basis.

What are your daily overhead fixed expenses? Those include your occupancy cost (rent, lease, or mortgage payment), utilities, equipment leases, staffing, employee costs, insurance—anything that continues to incur an expense whether you are seeing patients or not. Add up all these fixed expenses.

When you start to analyze your costs, you may discover that you need to raise your fees, based on operational costs. If your customary fees are too low, it affects your ability to negotiate with insurance companies because they know what your fees are. They know the fee schedule because either they receive claims with your usual fees on it, or they get that information from another insurance company (they share information). Not only do they know what you charge, they know what the common fees are in your geographic location by zip code.

It’s hard to ask an insurance company for $1,000 for a crown if your customary fee is only $900, and they know it. If your usual fees aren’t high enough, you can’t expect the insurance company to give you a pay raise. You may want to increase your fees a year or so before you even start to look at joining a PPO.

3. Understand Their Fees

After determining your fees and reaching out to potential PPOs, the first thing to look at is their fee schedule. Look at fees for the procedure codes that are most commonly billed by your office. For our practice, that includes hygiene fees, cleanings, exams, X-rays, composites, and crown-and-bridge fees. If a PPO-insurer pays 100 percent of a fee for root canals, but you don’t do root canals, that fee is meaningless.

The most commonly billed fee has the greatest impact overall. A small change in that fee over the course of a year can have a big impact.

4. Legal Implications

Fees are not the only factors to consider. Ask an attorney to analyze the contract before you sign it. Often, state dental societies have already done contract analyses. The lawyers on retainer for the dental society may have already performed a contract analysis that you can request.

When negotiating with PPOs, I’ve learned that, with the exception of the fee schedule, the standard insurance contract can’t be changed. Therefore, be aware of what you’re signing and understand exactly what that means to your practice going forward.

Evaluate fees and contracts independently. You may look at the fees and think they are acceptable, but then your attorney may advise against signing the contract for other reasons.

Another factor to be aware of is subcontracting (“selling your practice”) to another insurance company. If that happens, you may end up with a fee schedule that is different than what you anticipated, even though many times it doesn’t change.

Some companies will disclose that you will be contracted with multiple companies, but other contracts may make that information more difficult to recognize. Every dentist should be aware that it’s a possibility to be subcontracted to another insurance company, and should ask about it if it’s not clear.

Sometimes dentists think they’re signing a contract with a particular insurance company, but they’re actually signing with a third party who does the contracting for a number of insurance companies.

Another legal issue to be keenly aware of is the length of the contract. How long does it take to (without prejudice) get out of the contract? Is there a 60-day out or a 90-day out? Typically, contracts last a year and are self-renewing. But dentists can usually get out of any of these contracts within a specified amount of time.

5. Other Considerations

In addition to legal factors, there are other practical considerations. For example, if you’re seeing full-fee patients who happen to have coverage with a PPO you are considering, those patients will likely be converted to PPO patients after you join the program. Investigate how many of your existing patients will be covered by any insurance plan you consider. It may seem worthwhile to accept lower fees in order to increase your patient base, but not if half your full-fee patients suddenly become lower-fee patients.

On the other hand, if you’re not seeing any patients covered by a plan you are considering, joining that group may be a good way to grow the practice. A benefit from increasing your new patient flow is a corresponding increase in referrals. The more new patients that come into the practice, the more people who will refer their friends and relatives to you.

Another consideration is how many people an insurer covers in your area. It’s not worth your while to sign up with a company that only insures a hundred people in your area—you probably won’t see any new patients from such a small number of prospective patients.

On the other hand, if there’s a factory next door that has 6,000 employees, signing up to accept the insurance they offer provides much greater potential for increasing business.

The number of participating dentists in your area is also an important consideration. If the potential number of patients is small, and the number of dentists who already participate with a PPO plan is large, you may not get many new patients.

You can learn which dentists in your area participate with a particular plan by logging onto the PPO websites. Many insurance companies offer a tool to find a participating dentist in a certain locale on their websites. If you know any of those practicing dentists, ask them about their experience with that particular insurer.

Also, consider whether the specialists you work with will take the prospective insurance plan. Will signing up with one provider mean that you can’t refer your patients to your preferred specialists?

At first glance, joining a PPO has more considerations than many dentists might think. Go through the process slowly. Learn how working with these PPO companies impacts your practice by adding one at a time, if that’s what you want to do.

6. Ask Questions and Know Your Limits

As I began researching PPOs, I was surprised to learn that some insurance companies are flexible with their fees. When the insurance company reaches out to you (rather than you reaching out to them), you have better leverage in negotiating for a better fee schedule. Typically, the people you talk to are customer service people who are trying to build their network of providers, and sometimes they are willing to negotiate. It doesn’t hurt to ask.

After talking with several customer service agents, I learned that if I said I was interested but the fees were not high enough, I was often later offered two or three additional upgraded fee schedules. Sometimes those small, incremental changes were very significant. Other times, it still wasn’t worth it.

As with any negotiations, you have to be willing to walk away if they don’t offer what you feel is fair compensation. With one company, I was almost ready to sign up, but I asked them for an addition $10 per cleaning. Initially they said they couldn’t do it. I thanked them for their time and walked away. About two weeks later they came back and said they could do it.

If you know your numbers and you know exactly what you can and cannot accept in a fee proposal, it makes the process much easier.

7. Beware of Cost-Cutting Practices

The last thing to know is that PPOs sometimes deny treatment when you send in a claim because they recommend a lower-cost service for the patient. The amended treatment may indeed be less expensive to the insurance company and to the patient, but the quality of care may not be as high or as beneficial.

For example, you might place a crown for a patient, but the insurance company decides the crown was unnecessary and a filling should have been done instead. Even though you have already delivered the crown, the insurance company says you are only allowed to collect a fee for a filling. Contractually, some of those plans have the ability to do that.

To find out if a particular PPO tends to approve lower-cost procedures after a higher quality of care has been provided, talk to colleagues who have partnered with that PPO and ask about their experience. Do your research on the policies of each company before you sign on the dotted line.

8. Know Your Worth

For me, the bottom line is if compensation is so low that you start to think about cutting the quality of your care, then you shouldn’t take it. That may sound silly, but it’s not worth it to me if the PPO restricts my ability to provide the highest quality of care for people. Of course, it’s possible to provide quality care even if you get grossly under-compensated, but you have to do it at a loss.

At the end of the day, a dentist is running a business. You can’t function at a loss in your business and take care of anyone. Part of taking care of your patients includes taking care of your team members. If you’re not being compensated enough to be able to invest in your team members and have them grow professionally and personally, then you likely shouldn’t do it.

Conclusion

After the threat of losing 35 percent of my patients, I was compelled to investigate other PPO options. Today, my practice participates in three PPOs. They offer reimbursement at levels high enough that I am comfortable taking them.

In the past three years, we have expanded our practice to include a third dentist, so there was room in the schedule for new business. The third PPO provider helped us to attract new patients we had never seen before.

I had prepared for the worst-case scenario by considering what would happen if we lost a lot of our patients due to a 25 to 30 percent decrease in fees. But that insurer was regulated by the state to only a 9 percent decrease in their fees, and we kept most of those patients. I plan to renew our contract with that provider, knowing I can change my mind in 90 days if it is not working. We now have enough alternatives in place to mitigate any potential damage.

When we dropped out of many of these programs 15 years ago, a lot of patients left our practice to go to another participant. But we learned that a huge percentage of them eventually came back because they realized they weren’t being treated the same way that we had treated our patients.

When they returned, they came back as full-fee patients, not PPO patients. The most important thing is to provide the best quality dental care you are capable of providing, and make sure the practice earns enough to continue that legacy.